For the past six months, Washington State has been

experiencing the lowest unemployment rate in over 50 years. Washington has

gained over 83,000 jobs, across both the public and private sectors since April 20181. In such a competitive environment for talent, what are you doing to differentiate your organization and attract and retain the best and brightest candidates?

The answer doesn’t have to be terribly complicated; the most effective strategies are based on simply understanding your workforce and building a responsive benefits package. However, knowing what is important to your employees and, even more crucially, translating those needs into valuable program offerings requires careful data analysis and some thinking outside of the box.

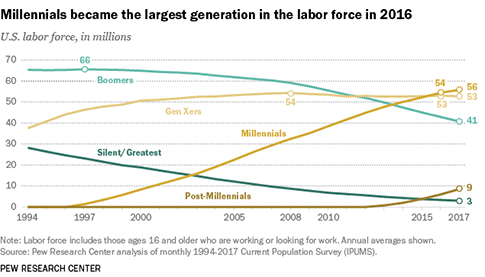

Millennials – the largest generation in the U.S. labor force2

Compared to other generations, millennials have a disproportionately

high amount of student loan debt. Among 18-29 year olds, it makes up almost 40% of all debt nationally3.

This financial burden has pushed many millennials to not contribute to traditional 401(k) plans, which commonly include employer matches. Only 52% of millennials are opting into these employer-sponsored retirement plans4. In addition to missing out on the opportunity to save for retirement, many are also leaving dollars on the table by way of employer-matched contributions.

401(k) matching contributions have long been known as valuable tool to boost retention5. Unfortunately, when the incoming labor force doesn’t take advantage of it, the program loses impact. So how can we redirect employees towards these programs?

What can employers do?

Abbott Laboratories, a medical research and development

company, proposed a creative solution last year. They amended their existing 401(k) plan to provide a 5% employer contribution towards an employee’s 401(k) plan if the employee was also making at least a 2% contribution towards student loan repayment.

They requested a ruling from the IRS, which responded in a Private Letter Ruling (PLR) that the proposed change would not violate the contingent benefit prohibition of section 401(k)(4)(A) and section 1.401(k)-1(e)(6)6. Since then, other companies have followed suit and began to integrate student loan benefits with their 401(k) programs, such as The Travelers Companies’ Paying it Forward Savings Program7. These programs strike a chord with the notoriously difficult to retain millennials, allowing them to contribute to their retirement while paying off their existing debt.

The IRS’ contingent benefit rule says that employers cannot

make other benefits, such as stock options or other entitlements, available

based on whether or not an employee makes 401(k) contributions. However, in

this case, it is the student loan contribution that triggers the 401(k)

contribution, thus not breaching the requirement.

Even with this ruling, there are several considerations that

employers should take into account before following suit and setting up a

similar program to attract and retain top talent, including nondiscrimination

testing requirements and eligibility questions.

Alternative strategies

Sound complicated? It is. Other employers seeking to avoid bureaucratic obstacles have set up standalone plans that simply direct funds towards each eligible employee’s student loans every month as an offering in their benefits package. This approach still reduces financial stress and provides a tangible benefit to indebted millennials, even though it does not contribute to the employee’s retirement.

Regardless of whether your employees have student loan debt or not, implementing a program that reduces your population’s financial anxiety

remains an extremely powerful retention tool. But it is important to first take the time to understand where that anxiety is stemming from, and design a responsive plan to those needs. The objective is to help your employees come to work and focus on exactly that – work, not how they are going to make ends meet. This provides a higher level of productivity and engagement from your workforce, as well as loyalty from the employees who want to grow and develop within a company that supports higher education. Call an experienced employee benefits broker to learn more about student debt relief and designing a valuable program.

The views and opinions expressed within are those of the author(s) and do not necessarily reflect the official policy or position of Parker, Smith & Feek. While every effort has been taken in compiling this information to ensure that its contents are totally accurate, neither the publisher nor the author can accept liability for any inaccuracies or changed circumstances of any information herein or for the consequences of any reliance placed upon it.

Disa Davis | Account Executive

Disa Davis | Account Executive